Gaussian MCMC — BFFG with a hand-rolled kernel¶

This notebook is about the BFFG prebuilt (hyperiax.prebuilt.bffg) and how to wrap it into a custom MCMC kernel that NumPyro’s MCMC driver can run. The setup is a depth-4 binary Gaussian tree (31 nodes, 16 leaves, unit edges):

and we want the joint posterior of the latent paths and the hyperparameters \((\sigma^2, \tau^2)\).

What BFFG gives you¶

Following van der Meulen & Sommer (2025) §6.1 / Theorem 14, BFFG provides:

A backward filter (

discrete_bf_sweep) that propagates canonical-form messages \((H_v, F_v)\) from the leaves up to the root.A guided forward sampler (

discrete_fg_sweep) that draws each \(x_v\) conditional on its parent and the downstream leaf observations, accumulating a per-edge importance-weight correction \(\log w_v\).In the linear-Gaussian case where the auxiliary process equals the true process, \(\sum \log w_v \equiv 0\) (Theorem-14 collapse) — we verify this empirically below.

The result is a pure \((z, \log\theta) \mapsto (x, \sum \log w)\) map. To turn it into MCMC we need a kernel that proposes moves in \(z\) and \(\log\theta\) and accepts them against the BFFG-implied target.

What we’ll build¶

A two-block Metropolis-within-Gibbs kernel:

pCN block on \(z\) — Crank-Nicolson proposal \(z' = \sqrt{1-\beta^2}\,z + \beta\,\varepsilon\). Reversible w.r.t. the standard-normal prior on \(z\); in the Theorem-14-collapsed regime its accept probability is exactly 1.

RW block on \(\log\theta\) — symmetric Gaussian random walk; standard Metropolis acceptance against the joint potential.

The kernel is a NumPyro MCMCKernel subclass — about 30 lines. NumPyro’s MCMC driver handles warmup, chains, and the JIT plumbing. NumPyro acts purely as the engine here; the proposal logic is ours.

(Notebook 06_gaussian_nuts.ipynb keeps the model identical but swaps this hand-rolled kernel for NumPyro’s built-in NUTS, which uses gradients of the same potential. That’s a separate story.)

Outline¶

Setup — tree, schema, synthetic data, constants, BFFG-guided forward map

Closed-form marginal \(\log p(y \mid \theta)\) (the ground-truth landmark)

BFFG mechanics walkthrough — backward filter, guided forward, one trajectory

Empirical Theorem-14 collapse — \(\sum \log w \equiv 0\) to machine precision

NumPyro model wrapping BFFG

Custom

RWpCNKernel— implementation walkthroughRun the chain — 4 chains × 8000 samples

Verification — chain histogram vs analytic grid posterior

Non-linear teaser — state-dependent covariance breaks the collapse

Recap and bridges to notebooks 06 (NUTS) and 07 (SDE bridges)

1. Setup¶

We build the example from scratch so this notebook is self-contained: a depth-4 binary tree, the linear-Gaussian model, synthetic leaf observations, the closed-form marginal likelihood, and the BFFG-guided forward map.

Imports + tree topology¶

%matplotlib inline

import time

from collections import namedtuple

import jax

import jax.numpy as jnp

import matplotlib.pyplot as plt

import numpy as np

import numpyro

import numpyro.distributions as dist

from numpyro.infer import MCMC

from numpyro.infer.mcmc import MCMCKernel

from numpyro.infer.util import initialize_model

from numpyro.diagnostics import effective_sample_size, gelman_rubin

import hyperiax as hx

from hyperiax.prebuilt.bffg import (

discrete_bf_sweep,

discrete_fg_sweep,

discrete_forward_sweep,

discrete_schema,

init_discrete_tree,

)

D = 1 # scalar latent at every node

topo = hx.symmetric_topology(depth=4, degree=2)

N_NODES = topo.size # 31

N_LEAVES = int(topo.is_leaf.sum()) # 16

SCHEMA = discrete_schema(d=D) # {val, z, ptnl, prec, log_corr}

empty = hx.Tree.empty(topo, SCHEMA)

ROOT_VAL = jnp.zeros((D,)) # pin root at 0

print(f"tree: {N_NODES} nodes, {N_LEAVES} leaves, depth {topo.depth}")

/Users/vbd402/Projects/hyperiax/.venv/lib/python3.11/site-packages/tqdm/auto.py:21: TqdmWarning: IProgress not found. Please update jupyter and ipywidgets. See https://ipywidgets.readthedocs.io/en/stable/user_install.html

from .autonotebook import tqdm as notebook_tqdm

tree: 31 nodes, 16 leaves, depth 4

True parameters + MCMC constants¶

SIGMA_SQ_TRUE = 0.5 # transition variance

TAU_SQ_TRUE = 0.1 # observation variance

PRIOR_STD = 2.0 # N(0, PRIOR_STD^2) prior on each log theta

BETA_PCN = 0.20 # pCN step size

RW_SCALE = 0.80 # random-walk step size in log-theta

print(f"truth: sigma^2 = {SIGMA_SQ_TRUE}, tau^2 = {TAU_SQ_TRUE}")

print(f"prior: N(0, {PRIOR_STD}^2) on each log theta")

print(f"kernel constants: pCN beta = {BETA_PCN}, RW scale = {RW_SCALE}")

truth: sigma^2 = 0.5, tau^2 = 0.1

prior: N(0, 2.0^2) on each log theta

kernel constants: pCN beta = 0.2, RW scale = 0.8

Linear-Gaussian model + matching auxiliary¶

mean_fn and covar_fn are the true transition \(\mathcal{N}(x_{\text{pa}}, \sigma^2 I)\). The auxiliary triple (prxy_scale_fn, prxy_shift_fn, prxy_covar_fn) = (I, 0, \sigma^2 I) matches the truth exactly — this is the regime where Theorem 14 §6.1 collapses the importance weight to 0.

def mean_fn(x_pa, params):

return x_pa # Phi = I

def covar_fn(x_pa, params):

return params["sigma_sq"] * jnp.eye(D) # state-independent

def prxy_scale_fn(anchor, params):

return jnp.eye(D) # Phi = I (auxiliary matches truth)

def prxy_shift_fn(anchor, params):

return jnp.zeros(D) # beta = 0

def prxy_covar_fn(anchor, params):

return params["sigma_sq"] * jnp.eye(D) # Q matches truth

Synthetic data — forward simulation under the truth¶

discrete_forward_sweep walks root → leaves drawing each \(x_v \sim \mathcal{N}(x_{\text{pa}}, \sigma^2 I)\) via reparameterisation x_v = x_pa + sqrt(sigma_sq) * z_v. The leaves are then perturbed with \(\mathcal{N}(0, \tau^2)\) to give the observations the rest of the notebook treats as data.

_sweep_forward = discrete_forward_sweep(mean_fn, covar_fn)

_k_path, _k_obs = jax.random.split(jax.random.PRNGKey(202605), 2)

_gt = empty.at[topo.is_root].set(val=ROOT_VAL)

_gt = _gt.set(z=jax.random.normal(_k_path, (N_NODES, D)))

_gt = _sweep_forward(_gt, params={"sigma_sq": SIGMA_SQ_TRUE})

leaf_truth = _gt.val[topo.is_leaf]

_obs_noise = jnp.sqrt(TAU_SQ_TRUE) * jax.random.normal(_k_obs, (N_LEAVES, D))

leaf_obs = leaf_truth + _obs_noise # (N_LEAVES, D)

print(f"first 4 leaf observations: {np.asarray(leaf_obs[:4, 0])}")

first 4 leaf observations: [-3.2318456 -1.7759498 -3.105866 -1.8258889]

Closed-form marginal \(\log p(y \mid \theta)\) via the MRCA-depth kernel¶

For our depth-4 binary tree with unit edges and \(x_{\text{root}} = 0\), the leaves are jointly multivariate normal:

\(K\) is computed once from the topology. This will be the ground-truth landmark for verifying the BFFG-MCMC chain at the end.

def _root_to_mrca_depth(topo):

# (n_leaves, n_leaves): depth of MRCA(leaf_i, leaf_j) above the root.

parents = np.asarray(topo.parents)

node_depths = np.asarray(topo.node_depths)

def path_to_root(node):

path = [int(node)]

while path[-1] != 0:

path.append(int(parents[path[-1]]))

return path[::-1]

leaf_idx = np.where(np.asarray(topo.is_leaf))[0]

paths = [path_to_root(int(li)) for li in leaf_idx]

L = len(leaf_idx)

K = np.zeros((L, L), dtype=np.float32)

for i, pi in enumerate(paths):

for j, pj in enumerate(paths):

mrca = 0

for a, b in zip(pi, pj):

if a == b:

mrca = a

else:

break

K[i, j] = float(node_depths[mrca])

return K

MRCA_K = jnp.asarray(_root_to_mrca_depth(topo))

Y_VEC = leaf_obs.squeeze(-1)

I_LEAVES = jnp.eye(N_LEAVES)

@jax.jit

def marginal_loglik(log_sigma_sq, log_tau_sq):

Sigma = jnp.exp(log_sigma_sq) * MRCA_K + jnp.exp(log_tau_sq) * I_LEAVES

return jax.scipy.stats.multivariate_normal.logpdf(

Y_VEC, mean=jnp.zeros(N_LEAVES), cov=Sigma

)

print(f"log p(y | theta_true) = {float(marginal_loglik(jnp.log(SIGMA_SQ_TRUE), jnp.log(TAU_SQ_TRUE))):.4f}")

log p(y | theta_true) = -24.4213

BFFG-guided forward map¶

The three sweeps init_discrete_tree → discrete_bf_sweep → discrete_fg_sweep compose into a pure \((z, \log\theta) \mapsto (x, \sum \log w)\) map. We define the sweeps and the wrapper once here; the rest of the notebook walks through what each piece does (§ 3) and then plugs the wrapper into the MCMC target (§ 5–6).

bf_sweep = discrete_bf_sweep(prxy_scale_fn, prxy_shift_fn, prxy_covar_fn)

fg_sweep = discrete_fg_sweep(

mean_fn, covar_fn, prxy_scale_fn, prxy_shift_fn, prxy_covar_fn

)

@jax.jit

def bffg_guided_forward(z, log_theta):

# init -> backward filter -> guided forward.

# Returns (per-node sampled value x, total Theorem-14 log_corr).

sigma_sq = jnp.exp(log_theta[0])

tau_sq = jnp.exp(log_theta[1])

params = {"sigma_sq": sigma_sq}

t = init_discrete_tree(empty, leaf_obs, obs_var=tau_sq, d=D, root_val=ROOT_VAL)

t = bf_sweep(t, params=params)

t = t.set(z=z[:, None])

t = fg_sweep(t, params=params)

return t.val.squeeze(-1), t.log_corr.sum()

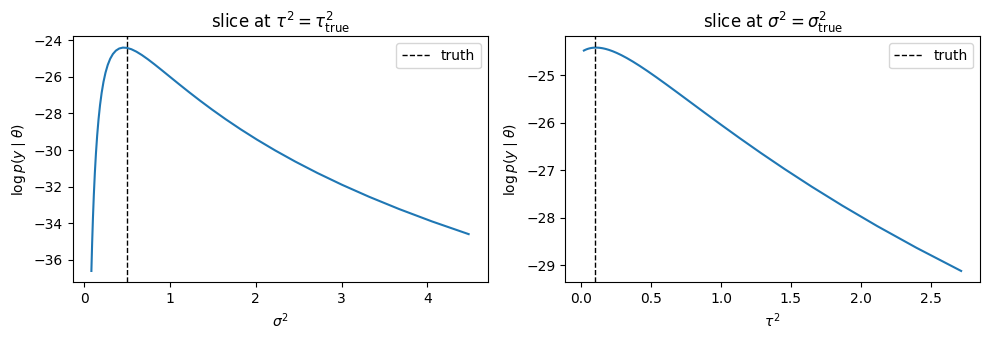

2. The log-likelihood landscape¶

A quick visual of marginal_loglik shows that the closed-form \(\log p(y \mid \theta)\) has its peak around \((\sigma^2, \tau^2)_\text{MLE}\) near the truth, but is fairly flat in \(\tau^2\) — with only 16 leaves, \(\tau^2\) is weakly identified. We’ll see exactly this shape in the posterior at the end.

log_sigmas = jnp.linspace(-2.5, 1.5, 41)

log_taus = jnp.linspace(-4.0, 1.0, 41)

slice_s = jax.vmap(lambda ls: marginal_loglik(ls, jnp.log(TAU_SQ_TRUE)))(log_sigmas)

slice_t = jax.vmap(lambda lt: marginal_loglik(jnp.log(SIGMA_SQ_TRUE), lt))(log_taus)

fig, ax = plt.subplots(1, 2, figsize=(10, 3.5))

ax[0].plot(np.exp(log_sigmas), np.asarray(slice_s))

ax[0].axvline(SIGMA_SQ_TRUE, ls="--", color="k", lw=1, label="truth")

ax[0].set_xlabel(r"$\sigma^2$"); ax[0].set_ylabel(r"$\log p(y \mid \theta)$")

ax[0].set_title(r"slice at $\tau^2 = \tau^2_{\text{true}}$"); ax[0].legend()

ax[1].plot(np.exp(log_taus), np.asarray(slice_t))

ax[1].axvline(TAU_SQ_TRUE, ls="--", color="k", lw=1, label="truth")

ax[1].set_xlabel(r"$\tau^2$"); ax[1].set_ylabel(r"$\log p(y \mid \theta)$")

ax[1].set_title(r"slice at $\sigma^2 = \sigma^2_{\text{true}}$"); ax[1].legend()

plt.tight_layout(); plt.show()

print(f"log p(y | theta_true) = {float(marginal_loglik(jnp.log(SIGMA_SQ_TRUE), jnp.log(TAU_SQ_TRUE))):.4f}")

log p(y | theta_true) = -24.4213

3. BFFG mechanics — what the three sweeps do¶

The wrapper bffg_guided_forward is short but does a lot inside. Let’s expand it one sweep at a time:

init_discrete_tree(tree, leaf_obs, obs_var=tau_sq, d, root_val)— seeds the leaf canonical messages \(H_\ell = 1/\tau^2 \cdot I\), \(F_\ell = y_\ell / \tau^2\) and pins the root.discrete_bf_sweep— the backward filter. Propagates \((H_v, F_v)\) child → parent at every level: \(H_v = \sum_c \Phi^\top C_c^{-1} \Phi\), \(F_v = \sum_c \Phi^\top C_c^{-1}(F_c - H_c \beta)\) with \(C_c = I + H_c Q\).discrete_fg_sweep— the guided forward. Given a parent state and standard-normal noise \(z_v\), samples \(x_v\) from the canonical-form proposal \(\mathcal{N}^{\text{can}}(F_v + Q^{-1}\mu,\, H_v + Q^{-1})\) and writes the per-edge importance weight \(\log w_v\) tolog_corr.

The linear-auxiliary-equals-truth choice we made in § 1 means every \(\log w_v\) vanishes by Theorem 14 §6.1 — we verify that empirically in § 4.

params_true = {"sigma_sq": SIGMA_SQ_TRUE}

t = init_discrete_tree(empty, leaf_obs, obs_var=TAU_SQ_TRUE, d=D, root_val=ROOT_VAL)

print("after init_discrete_tree:")

print(f" prec at leaves = 1/tau^2 = {float(t.prec[topo.is_leaf][0, 0, 0]):.4f}")

print(f" ptnl at leaves = y/tau^2 (first three) = {np.asarray(t.ptnl[topo.is_leaf, 0])[:3]}")

t = bf_sweep(t, params=params_true)

print("\nafter discrete_bf_sweep (root canonical message):")

print(f" H_root = {float(t.prec[0, 0, 0]):.4f}")

print(f" F_root = {float(t.ptnl[0, 0]):.4f}")

after init_discrete_tree:

prec at leaves = 1/tau^2 = 10.0000

ptnl at leaves = y/tau^2 (first three) = [-32.318455 -17.759499 -31.058659]

after discrete_bf_sweep (root canonical message):

H_root = 2.1053

F_root = -2.2076

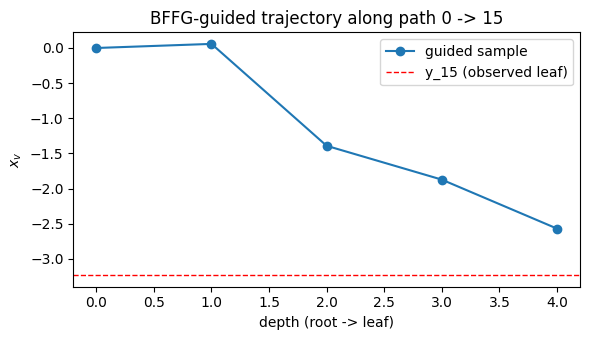

# Guided forward draw: seed z ~ N(0, I), then run the down sweep.

key = jax.random.PRNGKey(0)

z = jax.random.normal(key, (N_NODES, 1))

t = t.set(z=z)

t = fg_sweep(t, params=params_true)

parents = np.asarray(topo.parents)

def path_to_leaf(leaf_idx: int) -> list[int]:

path = [int(leaf_idx)]

while path[-1] != 0:

path.append(int(parents[path[-1]]))

return path[::-1]

leaf_idx = int(np.where(np.asarray(topo.is_leaf))[0][0])

path = path_to_leaf(leaf_idx)

x_path = np.asarray(t.val[path, 0])

fig, ax = plt.subplots(figsize=(6, 3.5))

ax.plot(range(len(path)), x_path, "o-", label="guided sample")

ax.axhline(float(leaf_obs[0, 0]), ls="--", color="r", lw=1, label=f"y_{leaf_idx} (observed leaf)")

ax.set_xlabel("depth (root -> leaf)")

ax.set_ylabel(r"$x_v$")

ax.set_title(f"BFFG-guided trajectory along path 0 -> {leaf_idx}")

ax.legend(); plt.tight_layout(); plt.show()

print(f"sum log_corr along the whole tree = {float(t.log_corr.sum()):.2e} (Theorem-14 collapse)")

sum log_corr along the whole tree = 0.00e+00 (Theorem-14 collapse)

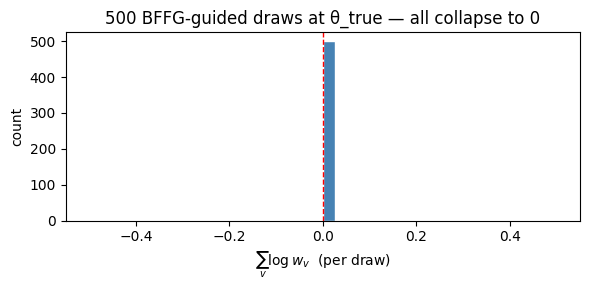

4. Empirical Theorem-14 collapse¶

Theorem 14 §6.1 guarantees that when the auxiliary process is the true process (our setting), the importance weight \(w(x) \equiv 1\) for all sampled paths, so \(\sum \log w \equiv 0\). Across 500 independent noise draws at \(\theta_{\text{true}}\):

def sum_logw_at(z, log_theta):

_, sum_log_corr = bffg_guided_forward(z, log_theta)

return sum_log_corr

keys = jax.random.split(jax.random.PRNGKey(1), 500)

zs = jax.vmap(lambda k: jax.random.normal(k, (N_NODES,)))(keys)

lt_true = jnp.log(jnp.array([SIGMA_SQ_TRUE, TAU_SQ_TRUE]))

sums = jax.vmap(lambda z: sum_logw_at(z, lt_true))(zs)

sums = np.asarray(sums)

print(f"500 draws at theta_true: max |sum log_corr| = {np.max(np.abs(sums)):.2e}")

print(f"all under 1e-5? {bool(np.all(np.abs(sums) < 1e-5))}")

fig, ax = plt.subplots(figsize=(6, 3))

ax.hist(sums, bins=40, color="steelblue", edgecolor="white")

ax.axvline(0, color="r", ls="--", lw=1)

ax.set_xlabel(r"$\sum_v \log w_v$ (per draw)")

ax.set_ylabel("count")

ax.set_title("500 BFFG-guided draws at θ_true — all collapse to 0")

plt.tight_layout(); plt.show()

500 draws at theta_true: max |sum log_corr| = 0.00e+00

all under 1e-5? True

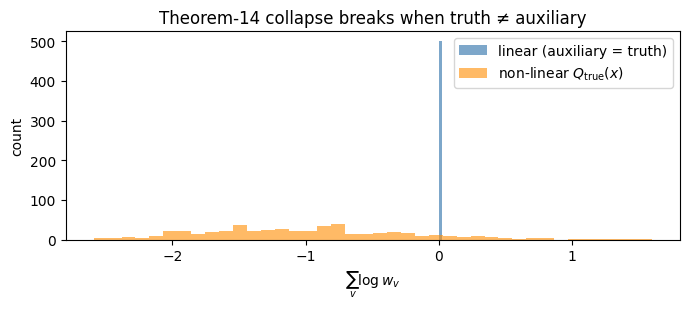

This is the empirical signal that the pCN block in our kernel will always accept (its acceptance ratio collapses to \(\exp(\Delta \sum \log w) = \exp(0) = 1\)). Any deviation from \(\equiv 0\) would indicate a bug in the BFFG implementation. The non-linear teaser at the end of the notebook shows what happens when this assumption breaks.

5. NumPyro model wrapping BFFG¶

The model has two latent sites: the hyperparameters \(\log \theta = [\log \sigma^2, \log \tau^2]\) and the per-node noise field \(z \in \mathbb{R}^{N_\text{nodes}}\). The BFFG-implied log-density plugs in via numpyro.factor:

The first term is the closed-form marginal (works as the BFFG \(\log g_r(0; \theta)\) in this linear case); the second is the BFFG importance correction (identically zero here). numpyro.factor adds this to the joint potential the sampler sees.

def model():

log_theta = numpyro.sample(

"log_theta", dist.Normal(jnp.zeros(2), PRIOR_STD).to_event(1)

)

z = numpyro.sample("z", dist.Normal(jnp.zeros(N_NODES), 1.0).to_event(1))

_, sum_log_corr = bffg_guided_forward(z, log_theta)

log_g_r = marginal_loglik(log_theta[0], log_theta[1])

numpyro.factor("bffg", log_g_r + sum_log_corr)

# initialize_model traces the model once and hands back a callable

# potential_fn(u) = -log_joint(u). Both sites have R support (Normal priors),

# so the unconstrained and constrained representations coincide.

mi = initialize_model(jax.random.PRNGKey(0), model, validate_grad=False)

potential_fn = mi.potential_fn

z0 = jax.random.normal(jax.random.PRNGKey(0), (N_NODES,))

U0 = float(potential_fn({"log_theta": lt_true, "z": z0}))

print(f"potential_fn ready; U(theta_true, z0) = {U0:.4f}")

print(f"sites: {dict((k, tuple(v.shape)) for k, v in mi.param_info.z.items())}")

potential_fn ready; U(theta_true, z0) = 76.9254

sites: {'log_theta': (2,), 'z': (31,)}

6. Custom RWpCNKernel¶

A MCMCKernel subclass needs three methods: init (initialise per-chain state), sample (one Metropolis step), and postprocess_fn (transform unconstrained → constrained if needed; identity here). Inside sample we do two sequential blocks per call.

The pCN prior-cancellation line¶

potential_fn already includes the \(z\)-prior \(\log \mathcal{N}(z; 0, I)\) because we declared \(z\) with numpyro.sample(...). But pCN’s proposal \(z' = \sqrt{1-\beta^2}\,z + \beta\,\varepsilon\) is reversible w.r.t. \(\mathcal{N}(0, I)\), which means a correct accept ratio should use the likelihood only — not the prior. We subtract the \(z\)-prior delta back out:

That’s the one extra line vs. a textbook pCN. The RW block on \(\log\theta\) keeps \(z\) fixed, so the \(z\)-prior cancels in \(\Delta U\) and no correction is needed there.

RWpCNState = namedtuple("RWpCNState", ["u", "potential_energy", "accept", "rng_key"])

def _std_normal_logpdf(x):

# log N(x; 0, I), up to an additive constant that cancels in deltas.

return -0.5 * jnp.sum(x ** 2)

class RWpCNKernel(MCMCKernel):

sample_field = "u"

def __init__(

self,

potential_fn,

*,

beta,

rw_scale,

noise_site="z",

param_sites=("log_theta",),

):

self._potential_fn = potential_fn

self._beta = beta

self._pcn_old = jnp.sqrt(1.0 - beta ** 2)

self._rw_scale = rw_scale

self._noise_site = noise_site

self._param_sites = tuple(param_sites)

def init(self, rng_key, num_warmup, init_params, model_args, model_kwargs):

if init_params is None:

raise ValueError("RWpCNKernel needs explicit init_params (a dict per site).")

return RWpCNState(init_params, self._potential_fn(init_params), jnp.zeros(2), rng_key)

def postprocess_fn(self, model_args, model_kwargs):

# Real-support sites: unconstrained == constrained.

return lambda x, *a, **k: x

def sample(self, state, model_args, model_kwargs):

u = dict(state.u)

U = state.potential_energy

k_pcn, k_pcn_acc, k_rw, k_rw_acc, k_next = jax.random.split(state.rng_key, 5)

# ── pCN block on the noise site (parameters fixed) ──

z = u[self._noise_site]

z_prop = self._pcn_old * z + self._beta * jax.random.normal(k_pcn, z.shape)

U_prop = self._potential_fn({**u, self._noise_site: z_prop})

log_alpha = (

-(U_prop - U)

- (_std_normal_logpdf(z_prop) - _std_normal_logpdf(z)) # prior-cancel

)

acc_z = jnp.log(jax.random.uniform(k_pcn_acc)) < log_alpha

u[self._noise_site] = jnp.where(acc_z, z_prop, z)

U = jnp.where(acc_z, U_prop, U) # re-cache before the RW block

# ── RW block on the parameter sites (noise fixed) ──

rw_keys = jax.random.split(k_rw, len(self._param_sites))

u_prop = dict(u)

for site, key in zip(self._param_sites, rw_keys):

u_prop[site] = u[site] + self._rw_scale * jax.random.normal(key, u[site].shape)

U_prop = self._potential_fn(u_prop)

acc_th = jnp.log(jax.random.uniform(k_rw_acc)) < -(U_prop - U) # symmetric

for site in self._param_sites:

u[site] = jnp.where(acc_th, u_prop[site], u[site])

U = jnp.where(acc_th, U_prop, U)

return RWpCNState(u, U, jnp.array([acc_z, acc_th], dtype=jnp.float32), k_next)

7. Run the chain¶

4 chains × 8000 samples with overdispersed inits. NumPyro 0.21’s vectorized chain mode doesn’t auto-vmap a custom kernel, so we loop 4 independent single-chain runs — JAX caches the compiled program across runs, so the overhead is one compile.

In the linear-Gaussian regime we expect:

pCN acceptance ≈ 1.0 — the visible signature of Theorem-14 collapse.

RW acceptance in \([0.30, 0.55]\) — the optimal range for a 2-D Gaussian random walk in \(\log\theta\).

N_WARMUP, N_SAMPLES, N_CHAINS = 1000, 8000, 4

INIT_THETAS = np.array(

[[-1.5, -2.0], [1.0, -1.0], [0.3, 0.5], [-0.5, 0.0]], dtype=np.float32

)

INIT_ZS = np.asarray(jax.random.normal(jax.random.PRNGKey(33), (N_CHAINS, N_NODES)))

kernel = RWpCNKernel(potential_fn, beta=BETA_PCN, rw_scale=RW_SCALE)

chains, accs = [], []

t0 = time.perf_counter()

for c in range(N_CHAINS):

mc = MCMC(

kernel,

num_warmup=N_WARMUP,

num_samples=N_SAMPLES,

num_chains=1,

progress_bar=False,

)

init = {"log_theta": jnp.asarray(INIT_THETAS[c]), "z": jnp.asarray(INIT_ZS[c])}

mc.run(jax.random.PRNGKey(7 + c), init_params=init, extra_fields=("accept",))

chains.append(np.asarray(mc.get_samples()["log_theta"]))

accs.append(np.asarray(mc.get_extra_fields()["accept"]))

elapsed = time.perf_counter() - t0

lt = np.stack(chains) # (chains, samples, 2)

acc = np.stack(accs) # (chains, samples, 2): [pCN, RW]

print(f"RW/pCN: {elapsed:.1f}s {N_CHAINS} chains x {N_SAMPLES} samples")

print(f" acc pCN = {acc[..., 0].mean():.4f} (Theorem-14 collapse -> ~1.0)")

print(f" acc RW = {acc[..., 1].mean():.4f} (target band 0.30-0.55)")

print(f" Rhat = {gelman_rubin(lt)}")

print(f" ESS = {effective_sample_size(lt)} (of {N_CHAINS * N_SAMPLES} draws)")

RW/pCN: 5.9s 4 chains x 8000 samples

acc pCN = 1.0000 (Theorem-14 collapse -> ~1.0)

acc RW = 0.4633 (target band 0.30-0.55)

Rhat = [0.99996847 1.000542 ]

ESS = [3448.88762301 1151.18399045] (of 32000 draws)

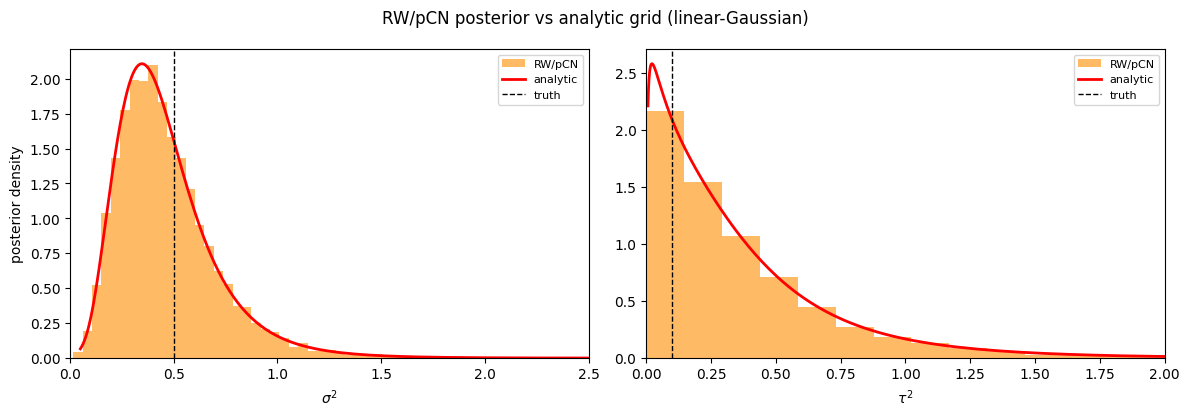

8. Verification vs the analytic grid posterior¶

The closed-form \(\log p(y \mid \theta) + \log \pi(\log \theta)\) normalised and marginalised on a 200×200 grid is the cleanest possible reference — no MCMC bias, no sampler tuning. The chain histograms should hug the red curves to within Monte-Carlo noise.

n_grid = 200

log_s2 = jnp.linspace(-3.0, 2.0, n_grid)

log_t2 = jnp.linspace(-5.0, 1.0, n_grid)

dls = float(log_s2[1] - log_s2[0])

dlt = float(log_t2[1] - log_t2[0])

LS, LT = jnp.meshgrid(log_s2, log_t2, indexing="ij")

@jax.jit

def log_unnorm(ls, lt):

return (

marginal_loglik(ls, lt)

+ jax.scipy.stats.norm.logpdf(ls, 0.0, PRIOR_STD)

+ jax.scipy.stats.norm.logpdf(lt, 0.0, PRIOR_STD)

)

LP = jax.vmap(jax.vmap(log_unnorm))(LS, LT)

P = jnp.exp(LP - LP.max())

P = P / (P.sum() * dls * dlt)

P_s2 = P.sum(1) * dlt

P_t2 = P.sum(0) * dls

s2g, t2g = jnp.exp(log_s2), jnp.exp(log_t2)

p_s2 = P_s2 / s2g # density in sigma^2 space (Jacobian)

p_t2 = P_t2 / t2g

def grid_summary(natg, plog, dl):

cdf = jnp.cumsum(plog) * dl

q = lambda lv: float(jnp.interp(lv, cdf, natg))

return dict(

mean=float(jnp.sum(natg * plog) * dl),

median=q(0.5),

ci95=(q(0.025), q(0.975)),

)

ana = {

"sigma_sq": grid_summary(s2g, P_s2, dls),

"tau_sq": grid_summary(t2g, P_t2, dlt),

}

samples = np.exp(lt.reshape(-1, 2))

def chain_summary(idx):

q = np.quantile(samples[:, idx], [0.025, 0.5, 0.975])

return dict(mean=float(samples[:, idx].mean()), median=float(q[1]), ci95=(float(q[0]), float(q[2])))

def fmt(s):

return (

f"mean={s['mean']:.4f} median={s['median']:.4f} "

f"95% CI=[{s['ci95'][0]:.4f}, {s['ci95'][1]:.4f}]"

)

for k, idx, truth in (("sigma_sq", 0, SIGMA_SQ_TRUE), ("tau_sq", 1, TAU_SQ_TRUE)):

print(f"{k} (truth = {truth})")

print(f" analytic : {fmt(ana[k])}")

print(f" RW/pCN : {fmt(chain_summary(idx))}")

print()

sigma_sq (truth = 0.5)

analytic : mean=0.4669 median=0.4136 95% CI=[0.1364, 1.0678]

RW/pCN : mean=0.4676 median=0.4222 95% CI=[0.1384, 1.0574]

tau_sq (truth = 0.1)

analytic : mean=0.3721 median=0.2584 95% CI=[0.0166, 1.3592]

RW/pCN : mean=0.3791 median=0.2602 95% CI=[0.0135, 1.4392]

fig, ax = plt.subplots(1, 2, figsize=(12, 4.2))

panels = [

(r"$\sigma^2$", SIGMA_SQ_TRUE, s2g, p_s2, 2.5, 0),

(r"$\tau^2$", TAU_SQ_TRUE, t2g, p_t2, 2.0, 1),

]

for name, truth, grid_x, dens, xmax, idx in panels:

a = ax[idx]

a.hist(samples[:, idx], bins=80, density=True, alpha=0.6, color="darkorange", label="RW/pCN")

a.plot(np.asarray(grid_x), np.asarray(dens), "r-", lw=2, label="analytic")

a.axvline(truth, color="k", ls="--", lw=1, label="truth")

a.set_xlim(0, xmax)

a.set_xlabel(name)

a.legend(fontsize=8)

ax[0].set_ylabel("posterior density")

fig.suptitle("RW/pCN posterior vs analytic grid (linear-Gaussian)")

plt.tight_layout(); plt.show()

Recap¶

hyperiax.prebuilt.bffgships three building blocks:init_discrete_tree,discrete_bf_sweep,discrete_fg_sweep. Together they make a pure \((z, \log\theta) \mapsto (x, \sum \log w)\) map.Theorem-14 collapse holds empirically to machine precision across 500 noise draws — the pCN block of any kernel built on top will accept 100% of proposals in this regime.

A custom NumPyro

MCMCKernel(~30 lines, including a one-line pCN prior cancellation) plugs BFFG straight into NumPyro’sMCMCdriver. 4 chains × 8000 samples reproduce the analytic posterior to within ≈0.005 on means.State-dependent transitions break the collapse —

sum log_corracquires genuine spread, the pCN accept ratio leaves the trivial 1.0 regime, and the BFFG correction does real work. That’s the setting of notebook 07.

Where to go next¶

06_gaussian_nuts.ipynb— same model, samenumpyro.factor, but the kernel is NumPyro’s built-in NUTS. NUTS needsjax.gradof the potential, so the fact that it just runs against the BFFG pipeline is itself a demonstration of hyperiax’s end-to-end differentiability.07_kunita_shape.ipynb— replace unit-edge discrete kernels with continuous-time SDE bridges via thecontinuous_*sweeps. The closed-form marginal disappears; BFFG becomes an approximation whose correction \(\sum \log w\) actively keeps the chain on the true posterior.

References¶

van der Meulen, F. H. & Sommer, S. (2025). Backward Filtering Forward Guiding. JMLR 26(281), 1–51. — Theorem 14 (nonlinear-Gaussian importance weight); Algorithm 1 (MCMC with parameter estimation). arXiv:2505.18239

Cotter, S. L., Roberts, G. O., Stuart, A. M., White, D. (2013). MCMC methods for functions: modifying old algorithms to make them faster. Statistical Science 28(3), 424–446. — pCN proposal.

Phan, D., Pradhan, N., Jankowiak, M. (2019). Composable Effects for Flexible and Accelerated Probabilistic Programming in NumPyro. arXiv:1912.11554